Economic Review February 2026

| Office for National Statistics reported subdued late-2025 growth, but PMI signals stronger first-quarter expansion | Inflation fell to 3.0%, raising expectations that Bank of England may cut rates soon | FTSE 100 reached record highs as public finances posted a surprise January surplus |

Survey highlights signs of encouragement

Although Office for National Statistics (ONS) figures released last month did reveal that the UK economy barely grew in the fourth quarter of 2025, a closely-watched survey suggests the economy has enjoyed a more encouraging start to this year.

The latest gross domestic product (GDP) statistics showed that UK economic output rose by 0.1% in the final three months of last year, the same lacklustre pace of growth as recorded during the third quarter. This figure was just below the consensus forecast from a Reuters poll of economists, with the underperformance partly reflecting a downward revision to November’s previously published monthly growth rate.

ONS described the overall picture of growth towards the end of last year as ‘subdued,’ noting there was no quarterly growth at all in the dominant services sector for the first time in two years. The construction sector was also weak, suffering its worst quarterly performance in four years, with the small overall fourth-quarter GDP increase driven entirely by growth from the manufacturing sector.

Evidence from a recently released economic survey, however, revealed signs of growing economic momentum across the first two months of this year, with the preliminary headline growth indicator from February’s S&P Global UK Purchasing Managers’ Index (PMI) rising to 53.9. This was a slight improvement on January’s final reading and the highest recorded level since April 2024.

S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said, “The early PMI data for February bring further signs of an encouraging start to the year for the UK economy. A solid rise in output across manufacturing and services has been reported in both January and February, with the rate of expansion gaining pace. The survey data so far this year are consistent with GDP rising by just over 0.3% in the first quarter if this performance is sustained into March.”

Inflation decline boosts rate cut hopes

Release of the latest consumer price statistics showed UK headline inflation is now sitting at a 10-month low, adding to expectations that Bank of England (BoE) policymakers will sanction another reduction in interest rates soon.

Data published last month by ONS revealed the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – fell to 3.0% in January. While this did represent a sizeable drop from December’s figure of 3.4%, the decline was actually in line with analysts’ expectations.

ONS said January’s slowdown was partly driven by a decrease in motor fuel prices, while the food and non-alcoholic drink sector also provided downward pressure, as did airfares, with prices in this category falling back after rising in December. The data also showed that these factors were partially offset by an increase in the cost of hotel stays and takeaways.

The latest inflation figures, along with other data released last month highlighting further jobs market weakness, increased the prospect of another reduction in interest rates when the BoE’s Monetary Policy Committee (MPC) next convenes later this month. At its previous meeting, which concluded on 4 February, the nine-member panel voted to leave rates on hold, as had been widely expected. Analysts noted, however, that the narrow five to four majority was a dovish surprise.

Minutes to February’s meeting also stated that Bank Rate ‘is likely to be reduced further’ and, in recent comments to the Treasury Committee, BoE Governor Andrew Bailey confirmed that a cut in March was a possibility if further evidence of easing inflation emerges. The outcome of this month’s MPC meeting will be announced on 19 March, with a recent Reuters poll showing a majority of economists expects policymakers to vote in favour of another quarter-point cut to Bank Rate.

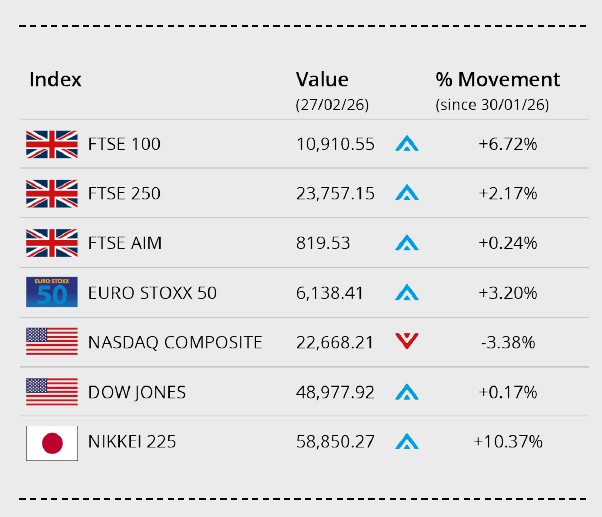

Markets

At month end, the UK blue chip FTSE 100 index outperformed US and European counterparts, closing a record-breaking week at another new high. The index closed the month up 6.72%, on 10,910.55.

Also in the UK, the mid-cap focused FTSE 250 ended February 2.17% higher on 23,757.13 and the FTSE AIM recorded a small 0.24% gain to close the month on 819.53. The Euro Stoxx 50 closed the month over 3% higher on 6,138.41. In Japan, the Nikkei 225 closed out February on 58,850.27, gaining over 10% in the month, supported by renewed optimism surrounding the Japanese economy and corporate sector.

US markets ticked lower at month end as a jump in wholesale prices fuelled concerns over a stubborn inflationary environment. The Dow Jones closed the month up around 0.17% on 48,977.92. The NASDAQ registered a monthly loss of 3.38% to close on 22,668.21.

On the foreign exchanges, the euro closed the month at €1.13 against sterling. The US dollar closed at $1.34 against sterling and at $1.18 against the euro.

Gold closed February trading around $5,251 a troy ounce, a gain of over 6% in the month, as investors seek safe haven assets – with US / Middle East developments keeping markets on edge. Brent Crude closed the month at around $72 a barrel, recording a monthly gain of over 10%. Tension between the US and Iran has heightened fears of disruption to oil flows through the Strait of Hormuz.

Public finances post record monthly surplus

The latest public sector finance statistics revealed a higher-than-expected budget surplus providing a boost for the Chancellor as she prepares to deliver her Spring Forecast.

ONS data showed that UK public sector net borrowing (the gap between the country’s overall income and expenditure) recorded a record monthly surplus of £30.4bn in January 2026. This figure, which topped all forecasts in a Reuters poll of economists, was double last January’s surplus, as stronger Income Tax, employers’ National Insurance contributions and Capital Gains Tax receipts, as well as lower debt interest payments, buoyed the government’s finances.

As a result, total borrowing across the first ten months of the current financial year now stands at £112bn, almost £15bn less than the same period last year. This figure is also significantly below the Office for Budget Responsibility’s (OBR’s) November forecast of £120bn for the same period.

On 3 March, the Chancellor will provide an update on the country’s finances in her Spring Forecast. A new OBR forecast for economic growth and the public finances will be published alongside her forecast, although the OBR will not provide a formal assessment of whether the Chancellor is on track to meet her fiscal rules.

Retail sales rise strongly in January

While the latest official retail sales statistics revealed stronger-than-expected growth in sales volumes during the first month of this year, survey data continues to highlight a relatively tough environment for the retail sector.

Recently published ONS data showed that total retail sales volumes grew by 1.8% in January, a significant improvement on December’s 0.4% rise and much healthier than the 0.2% median forecast from a Reuters poll of economists. The release also revealed that sales volumes rose by 4.5% over the year to January; this represents the fastest annual growth rate in nearly four years.

ONS noted that January’s sales jump was driven by strong auction demand for artwork and antiques as well as a further rise in sales at online jewellers, both linked to the recent spike in gold and silver prices. An increase in demand for sports supplements driven by healthy new year’s resolutions also provided a boost to January’s figures.

The latest CBI Distributive Trades Survey, however, continues to highlight ‘gloomy sentiment’ across the retail and broader distribution sector. Indeed, data from last month’s survey suggests sales volumes fell back sharply in February, with retailers saying the unusually persistent wet weather discouraged shoppers from visiting stores.

All details are correct at the time of writing (02 February 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.